carried interest tax reform

Recently Congress passed 2017 Tax Reform and included a new provision meant to address the criticism that carried interests provide favorable tax treatment deferred gains that are treated as long-term capital gain which are taxed at 15 or 20 depending on a taxpayers filing status and taxable income for. The industry strongly opposed extending the holding period to three years as part of tax reform legislation enacted in 2017 but notes that final regulations released in January 2021 exclude Section 1231.

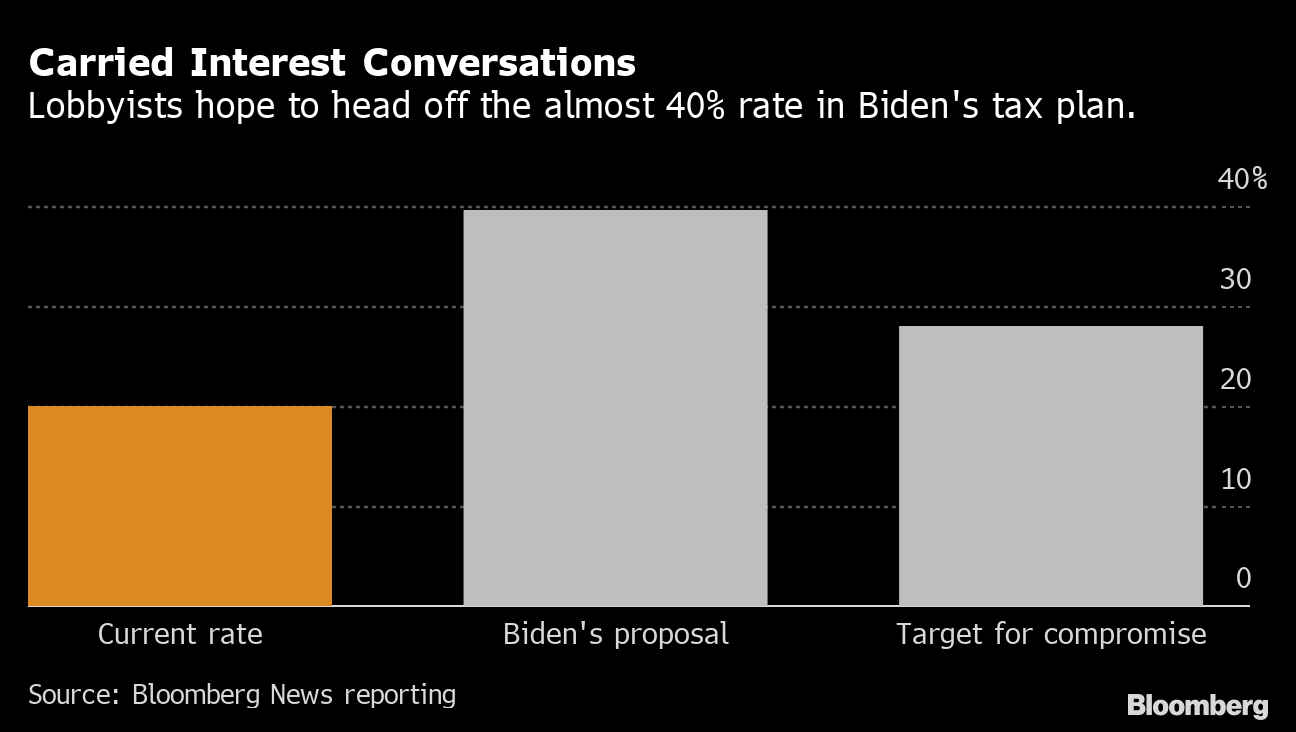

Carried Interest Tax Break Unites Pe Firms As Congress Takes Aim Bloomberg

New Code section 1061 is effective for taxable years beginning after 2017 and has changed the holding period for capital gains realized by a taxpayer who holds an applicable partnership interest as defined below.

. The Tax Cuts and Jobs Act of 2017 PL. Its only created when the fund generates profits. The loophole is called carried interest.

The Taxation of Carried Interest. Tax Rate and Business Tax Reform. Its usually tied to a specified rate of return known as profits over.

115-97 the Act enacted new Code section 1061. The Bill would consolidate the tax brackets for all individual taxpayers and reduce the maximum corporate tax rate to 20. WASHINGTON Fierce lobbying by the private equity industry is the reason the carried interest tax rate is not included in President Joe Bidens planned tax hikes top White House economist.

Section 1061 which was added to the Code as part of the 2017 Tax Cuts and Jobs Act provides that capital gains allocated to a carried interest holder will only be treated as long-term capital gains to the carried interest holder if the gain is derived from a sale or other disposition of a capital asset after a holding period of. These rules make some notable and mostly taxpayer-friendly changes to regulations proposed in July 2020. Carried interest also referred to as the carry which might entail 20 of the funds profits over a set period typically annual with the exception of private equity funds.

The carried interest loophole is an absurd mischaracterization of income that allows about 5000 of the richest people in America to divide conservatively 18 billion a year between themselves for an average tax break of 300000 a year. The carried interest loophole is yet another example of Wall Street executives exploiting our tax code to pad their pockets rather than invest in workers and Main Street said Senator Brown. Washington DC Rep.

Currently the managers of private investment partnerships are able to receive compensation for these services at the much lower capital gains tax rate rather that the ordinary income tax rate by. The alternative minimum tax AMT would be repealed for all taxpayers. The IRS released proposed regulations on July 31 2020 that would implement the three-year holding period requirement for holders of carried interests in a partnership.

Corporate greed is fundamental to the Wall Street business model and workers arent going to get their fair share until we change it. Understanding the Issues National Tax Journal 60 3. The best summation comes from the Patriotic Millionaires who said.

The Act increased the amount of time a general partner needed to hold their interest. NMHCNAA believe that carried interest should be treated as a long-term capital gain if the underlying asset is held for at least one year. The 2017 Tax Reform Increased the Carry Period.

Tax Reform Tax Arbitrage and the Taxation of Carried Interest Testimony before the US House of Representatives Committee on Ways and Means Washington DC September 6. The government released proposed regulations on July 31 2020 addressing the application of code section 1061 which was added as part of the Tax Cuts and Jobs Act of 2017 and is commonly referred to as the carried interest rules. What is a carried interest.

Generally section 1061 operates to recharacterize long-term capital gains into short-term capital gains taxed at. Thats tax jargon for the share of investors profits that goes to the managers of private. Closing corporate tax breaks and loopholes including the carried interest loophole individual private equity firms and the major trade group representing their industry the American Investment Council are investing in top tier lobbying talent to save their preferential tax treatment.

The Proposal would repeal Section 1061 1 the three-year carry rule that was enacted as part of the 2017 tax reform legislation and instead subject the holder of a carried interest to current inclusions of compensation income taxable at ordinary income rates in amounts that purport to approximate the value of a deemed interest-free. On January 7 2021 the Department of the Treasury and the IRS issued final regulations under Section 1061 of the Internal Revenue Code regarding the taxation of carried interests. 12 The private equity industry has spent over 25 million in lobbying since 2020 according to.

Fleischers piece which called the treatment of carried interest an untenable position as a matter of tax policy began a heated debate in Congress and tax policy circles on the topic. The three-year holding period for carried interests was introduced in Section 1061 of the Internal Revenue Code IRC as part of the tax reform law commonly known as the Tax Cuts and Jobs Act TCJA. One of the reasons that some of the controversy surrounding carried interest has died down in recent years was the passage of the 2017 Tax Cuts and Jobs Act TCJA.

Taxation of Carried Interest The current tax treatment of carried interest is the result of the intersection of several parts of the. The rate reductions would also be available for US. In 2014 Ways and Means Committee Chairman Dave Camp introduced a tax reform bill that would have raised rates on carried interest to 35 percent.

The Act was signed into law on Dec. Carried interest isnt guaranteed. Sander Levin today reintroduced legislation to tax carried interest compensation at the same ordinary income tax rates paid by other Americans.

Generally fixed as a percentage of assets the carried interest is variable because it is generally a share of fund profits once specified investment returns have been met ie subject to a hurdle rate. Tax-exempt investors subject to tax under the UBTI rules.

What Are The Green And Environmental Taxes Iberdrola

2

What Are The Consequences Of The New Us International Tax System Tax Policy Center

European Flag European Commission Brussels 22 12 2021 Com 2021 823 Final 2021 0433 Cns Proposal For A Council Directive On Ensuring A Global Minimum Level Of Taxation For Multinational Groups In The Union Swd 2021 580 Final

Tax And National Insurance Contribution Rates Low Incomes Tax Reform Group

2

Eu Hails G7 Tax Agreement But Internal Divisions Could Thwart Consensus Euronews

2

2

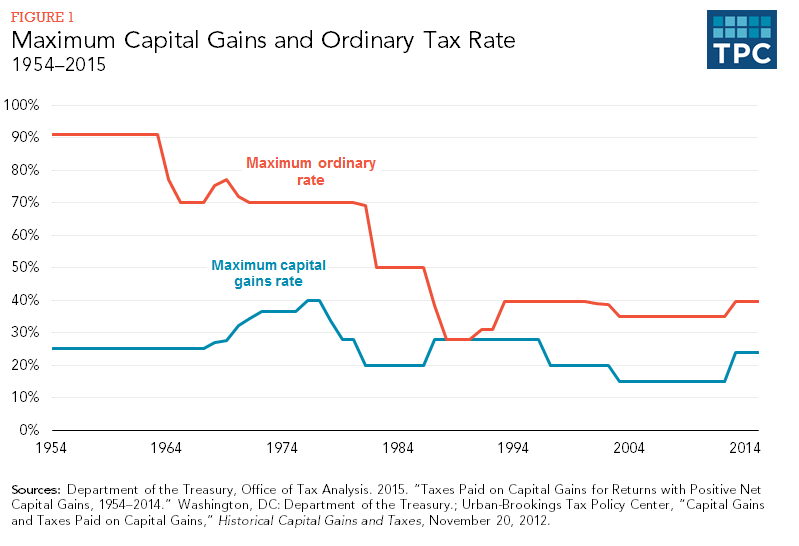

Capital Gains Full Report Tax Policy Center

Remote Work Tax Reform Improving Tax Mobility And Tax Modernization

Selling Your Home Low Incomes Tax Reform Group

Capital Gains Tax On Gifts Low Incomes Tax Reform Group

Pin On Tech News

/GettyImages-911586914-d4186dafdd8d4c3f94d4b0077f3c5918.jpg)

Explaining The Trump Tax Reform Plan

Carried Interest Tax Break Unites Pe Firms As Congress Takes Aim Bloomberg

How Does The Personal Representative Deal With The Income And Capital Gains Arising After The Deceased S Death Low Incomes Tax Reform Group

What Is E Way Bill Under Gst Goods And Services Internet Usage Goods And Service Tax

Capital Gains Tax Examples Low Incomes Tax Reform Group